One of the main regulations that banks have to comply with are capital requirements; in particular, banks need to hold a minimum amount of capital depending on the composition of their investments (assets). Actually, the use of the word “hold”, although quite common, is slightly misleading: capital is a source of funding for the bank—to be precise, an internal source of funding—so it is not something that banks hold, like cash. This short video discusses the concept.

There are several rationales for subjecting banks to such regulation. An obvious one is the fact that bank defaults (what happens when they run out of capital) impose very high costs to the economy; in other words, there are negative externalities that banks do not internalise. The way to design capital requirements, however, is far from obvious. In fact, just in 2007, right before the financial crisis, banks look sufficiently capitalised, at least according to the regulatory framework in place at that time. But they were not. Lack of liquidity, for instance, can lead to insolvency. Off-balance sheet exposures might become on-balance sheet very fast. Another lesson learned from the crisis was that risks build up during the boom and then materialise in the bust. Therefore, requirements should be increased during a boom—although it looks like risks are low—to protect the banking sector, and the real economy, when things go south.

One of the main new tools to deal with this time-varying dimension of financial risks is the Countercyclical Capital Buffer (CCyB). The idea is exactly as stated below: the macroprudential authority of the country should increase the buffer when the economy is doing well and reduce it in the opposite case. This post in the St. Louis Fed explains it well. For instance, right now, with the Covid-19 pandemic, is the moment to reduce it. The problem faced by many countries, however, is that they had not even activated in the first place. And this points towards a strong limitation of this tool that hopefully could be reformed in the near future.

As of October 2019, only 10 out of the 31 countries in Europe had positive CCyB. 6 of them had it at 1% or less. Only Sweden had a CCyB at its maximum level under European legislation, 2.5%, while Norway had it at 2%. UK had set it at 1%. The UK is, in fact, a good example to illustrate how the decisions to increase and decrease it are taken.

In its meeting in March 2016, the FPC—the macroprudential regulator in the UK—decided to increase the CCyB from 0% to 0.5%. Because it takes one year to become effective, the increase would take place in March 2017. However, after the EU referendum in June 2016, the FPC decided to bring it back to 0%. The reduction, contrary to the increase, is immediate. In other words, the CCyB never moved. There were no changes until July 2017, when the FPC increased it to 0.5% (effective July 2018) Then, in November 2017, it was decided to increase it to 1% (effective November 2018).

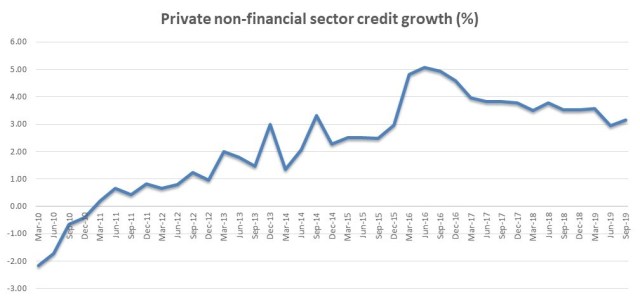

So what was the actual CCyB since January 2016 until March 2020? Well, it increased to 0.5% in July 2018 and to 1% in November 2018, coming back to 0% last month due to the pandemic. Hence, in the last four years, the UK had positive CCyB for just over a year and a half. And this in a period where credit was growing well…

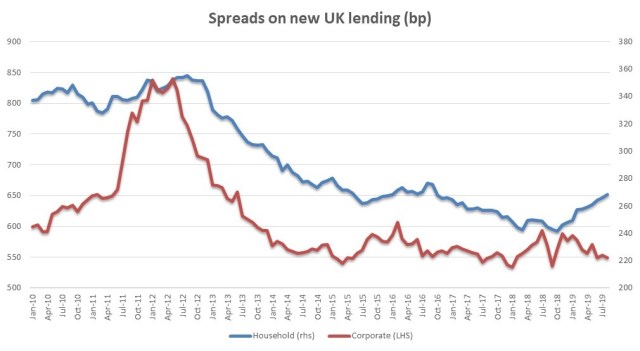

… and lending spreads were at their lowest since the financial crisis.

And the UK is one of the (few) countries that appears interested in using this tool. This situation looks quite opposite to the stance that regulators took early in the Basel III discussion times. In December 2009, the BCBS published a document presenting the proposals from the committee to strengthen the resilience of the banking sector. One of the points was dedicated to reducing the pro-cyclicality of the financial sector.

The financial sector can be very pro-cyclical. What that means is that, during a boom, the growth of the economy if even higher since the financial sector provides cheap credit; however, during the bust, the recession is deeper because the financial sector stops lending and potentially hoards cash. It turns out that some parts of the banking regulation actually increase this pro-cyclicality. Hence, it appeared important to re-design some aspects of it as well as providing some tools to mitigate the pro-cyclicality.

Among the potential re-designs there are things such as making the minimum capital requirements—i.e., those that are not increased or decreased through the cycle—less pro-cyclical. Repullo and co-authors showed that capital requirements for the same mortgage portfolio can vary up to 50% through the cycle. Although some changes have been introduced in Basel III—for instance, input floors—which should reduce pro-cyclicality, this was not their main goal.

Another proposal was the use of dynamic provisioning. This is a regulation that was introduced in Spain in the year 2000, and even though it was not enough to fully protect the banking sector, the consensus is that it saved a substantial amount of tax-payer’s money. Unfortunately, this idea was dropped early on at Basel, likely due to the strong heterogeneity among member countries regarding provisioning practices.

At last, we ended up with just countercyclical capital buffers, and with sever limitations. The maximum amount is 2.5% over RWAs. Yet, banks face at least a 7% requirement at all times—plus any supervisory addition—so the CCyB represents at most increasing requirements by a third. Given the volatility of credit cycles, coupled with the huge costs from financial crises, it is strange that this requirement is less than, say, 50% of total requirements.

But the other limitation is probably more serious: national authorities have discretion over when to activate it. Although it is difficult to come up with a set of rules about when to raise or reduce it, discretion has led to most countries having it at 0% before the Covid-19 pandemic, even though several countries in the EU were growing relatively well in the recent years.

How different would have been if, say, the CCyB could go up to 4-5% of RWA and national authorities would be required to increase it when credit is growing well? Many banking regulators would have room to free up bank capital which could be used to keep lending to firms with problems to repay, even if this increases credit risk. The opposite of what we have.

,_2019Q3.png){kind=link}

Pingback: Limiting borrowers leverage | Francesc's Blog