In the last post I talked about the countercyclical capital buffer (CCyB), a new regulatory tool to increase banks’ capital requirements that most countries have not used but that could have been effective to mitigate the Covid-19 crisis. As I mentioned there, the UK did use it, albeit not to the full extent. But the UK has used other tools to try to limit the buildup of risks; one of the most important ones is a tool limiting the number of high loan-to-income mortgages.

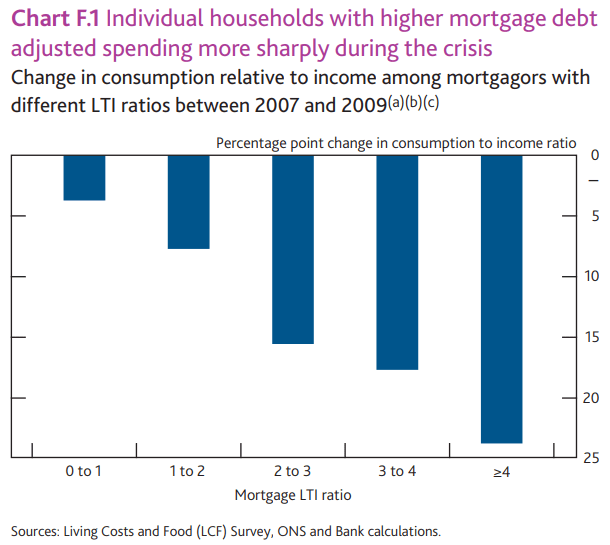

Loan-to-income (LTI) indicates how big is the mortgage debt relative to the annual income of the borrower. If someone earning £60,000 a year takes a £240,000 mortgage to buy a house, then the LTI is 4. The higher the LTI, the higher the leverage borrowers are taking. And the higher the amount borrowed with respect to income, the more consumption responds to changes in aggregate conditions. The reason is that borrowers adjust their consumption in order to reduce the possibility of default, especially in countries with full-recourse, such as the UK. The chart below presents evidence that higher LTIs were associated with stronger reductions in consumption during the financial crisis (even when normalising by income). The chart is taken from the Bank of England’s December 2019 Financial Stability Report.

Therefore, reducing mortgages with high LTIs should lead to a smaller adjustment during a crisis. I am not going to discuss here the differences between the Covid-19 and the financial crises—for instance, consumption is going down mostly because of the quarantine, not because unemployment is going up. The point is to highlight another measure introduced by the Bank of England in 2014: a limit on the number of mortgages with LTI equal or above 4.5 that lenders can grant. If this measure indeed limited this type of mortgages, then this might improve consumption during the Covid-19 crisis.

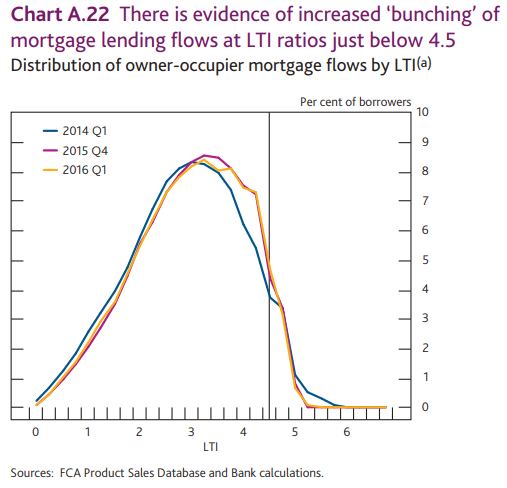

The evidence from the distribution of LTIs before and after the policy was introduced is consistent with the idea that it limited high LTI mortgage lending. In the chart below (taken from the July 2016 FSR) we can see that although the distribution has shifted right (compared to 2014Q1), the frequency of mortgages with LTI above 4.5 has decreased. To the extent that this reduction would not have happened without the policy (luckily we will share some evidence backing this claim up soon) then the adjustment in consumption during this crisis might be lower than what would have happened without the policy.

In general, one of the issues with this type of intervention (which we broadly call “macroprudential policy”), is that one can only empirically assess the “costs” while the economy is growing well; costs, for instance, would be a reduction in mortgage lending. It is precisely only during a crisis, or at least a change in the cycle, where the benefits of this policy start to show. This is one of the reasons why we see a weakening of the regulatory framework as the economy recovers and grows healthily. This Covid-19 crisis might in fact stop this trend and reinforce the importance of macroprudential regulation.